What Is a Memorandum of Understanding (MOU)?

An MOU is a preliminary agreement between the buyer and seller that outlines key terms, conditions, and timelines of the property sale. It helps protect both parties by clarifying responsibilities and expectations before signing the final contract.

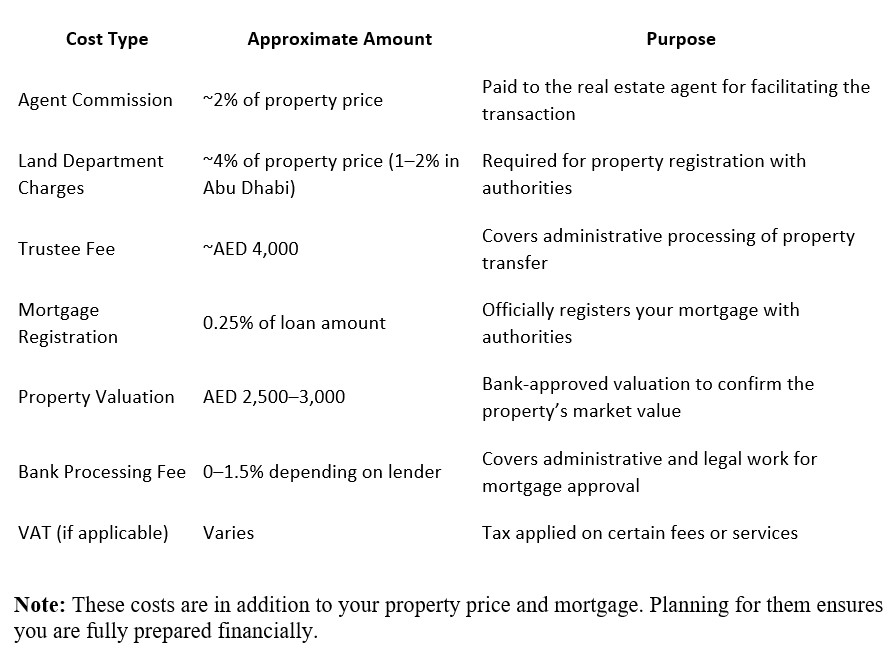

What Other Costs Should You Expect?

Can You Leave the UAE While Still Holding a Mortgage?

You can leave the UAE while still holding a mortgage, as long as all payments continue on time. Banks may require a local representative or proper communication channels to ensure timely repayment. Planning ahead helps avoid penalties or issues while abroad and ensures your mortgage remains in good standing.

What Does a Mortgage Broker Do?

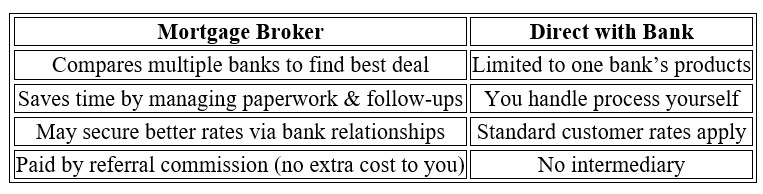

A mortgage broker is an independent professional who helps you find the most suitable mortgage for your needs. They compare multiple banks, explain the pros and cons of different options, and guide you through the application process, making it easier and faster to secure the right loan.

What Are the Advantages of Getting a Mortgage in the UAE?

Getting a mortgage in the UAE offers several benefits:

• High Rental Yields: Potential to earn strong rental income from your property.

• Property Appreciation: Real estate values may increase over time, growing your investment.

• Competitive Rates: Access to attractive interest rates from multiple banks.

• Flexible Payment Terms: Options to choose repayment plans that suit your budget and timeline.

• Access to Modern Real Estate: Opportunity to invest in new, high-quality developments with modern amenities.

• High Rental Yields: Potential to earn strong rental income from your property.

• Property Appreciation: Real estate values may increase over time, growing your investment.

• Competitive Rates: Access to attractive interest rates from multiple banks.

• Flexible Payment Terms: Options to choose repayment plans that suit your budget and timeline.

• Access to Modern Real Estate: Opportunity to invest in new, high-quality developments with modern amenities.

Should I Use a Mortgage Broker or Go Directly to the Bank?

• Conclusion: Choosing a mortgage broker gives you the advantage of expert guidance, access to multiple banks, and better rates — making your mortgage journey faster, easier, and more financially rewarding than going directly to a single bank.